This next post is about Debt. I think this is one of the most important parts of investing. People can get hung up on how much or little Debt the company has, but it’s always important to dig deeper. The company could be opening new stores or launching a new website, sometimes there is an important reason that they have that Debt. For the people who like rules I want to stress that you, as an investor, needs to set your own comfortable boundaries. Some people are comfortable with more Debt. It depends if you don’t mind taking a risk or if you are a stay in the boat type of person.

When you hear the horror stories about companies closing down or when you walk by your favorite local restaurant and has spontaneously shut down, most of the time it’s because of Debt. Yes, sometimes if it’s a restaurant it might not be up to code, that could be because they couldn’t afford it. Why couldn’t they afford it? Because of Debt. Forbes says 8 out of 10 businesses fail because of lack of cash, otherwise know as Debt.

We all cringe when we hear the word Debt, even as a child I think I did. It’s a scary word, Debt can show how well the company is managing their money. The reason Debt is like being invited out for a Steven King movie marathon is because it’s your money. The money that is invested into a company isn’t your mom’s money, no, it’s your money and if the company messes up then it’s your money and lifestyle on the line. Debt causes bankruptcy. You lose your business and have to start everything from scratch if you choose to start again. As my father says, “ You have to make a mistake a day.” That would be your mistake, you can learn from it and improve for your future company.

I am making Debt sound like a horrible thing but it’s not always. Here are two examples of how Debt can either make or break your company.

Sara and Lily want to try to sell more lemonade than they did the first time. They ask their dad, Farhang to invest $16.00 in the lemonade stand instead of the normal $8.00. After selling $8.00 worth of lemonade it starts to rain. Lily and Sara have to close their stand and go inside. They pay Farhang back $8 of his $16. Because they lack the other half of his money, Lily and Sara now have $8.00 Debt. They did make the $8.00 in the next lemonade stand but due to the rain it took them a while to pay Farhang back. If Lily and Sara were dealing with a bank for loan along with the $8.00 they would have to pay interest.

That’s one way to look at Debt, now let’s look at the other.

Lily and Sara feel like they’ve done so well with the one lemonade stand that they wanted to invest in more stands. They had to pay for two tables, $60.00, triple the cost of the ingredients, $24.00, and one quarter of the Profit. Because they only make $2.00 per lemonade stand they will be $84.00 in Debt.

Both stories cause Debt but one will be easier to work out of then the other. In the first story because of an unexpected problem Lily and Sara lost money. It wasn’t their fault that they lost money. It was just something they didn’t prepare for, sometimes what can happen is if Lily and Sara’s stand has too many slip ups like that Farhang won’t invest in their stand any more because he will be unsure if he’ll get his money back. In the second story Lily and Sara decided to invest in two more lemonade stands this causes more Debt in the beginning but if they are as successful as the first stand they will soon pay it off.

Number of stands

|

Amount of Debt

|

Earnings

|

Amount of Debt Left

| |

Three Stands Scenario

|

3

|

$84.00

|

$6.00

|

-$78.00

|

One Stand Scenario

|

1

|

$8.00

|

$2.00

|

-$6.00

|

*** $2.00 per stand***

As you can see it can make sense to acquire Debt in some cases, sometimes you need to in order for your business to grow. Now let’s look how to measure Debt.

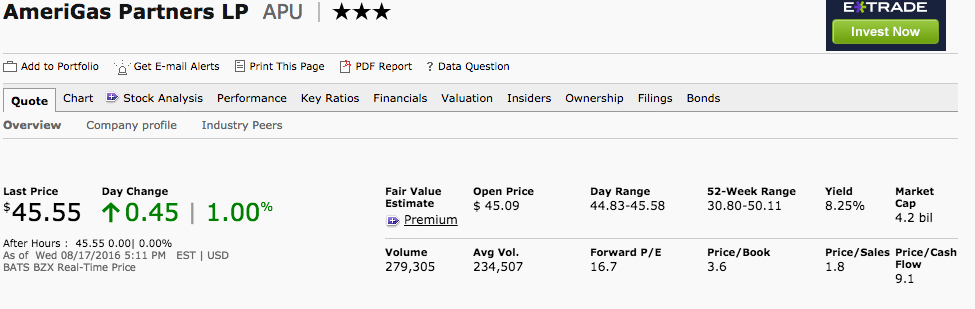

It’s hard to see but the metric we want is the Market Cap. You can see it in the top right corner. Here is it zoomed in.

It’s important to know how to calculate and use the Debt to Equity Ratio. Let’s look at the stock AmeriGas. Debt is how much money you still owe, and Equity is the value of the company, otherwise known as the Market Cap.

First we need to find the Debt to Equity Ratio. The website Morningstar gives us the Debt to Equity Ratio which is 2.0.

Secondly we have to find the Market Cap, which is 4.2 Billion dollars.

Next we have to divide the two to figure out the Ratio of Debt to Equity or the “x” value:

x / 4.2 Billion = 2.0

Then we would multiply 4.2 Billion by 2, that would give us 8.4 Billion dollars in Debt.

That is how much AmeriGas has in Debt. Again, depending on how risky of an investor you are, this might be too much Debt or maybe it’s just right on the line.

Another important thing investors should know about is Interest Coverage. On Morningstar you can find it at the bottom of the Key Ratios page. Interest Coverage is a ratio that shows how many years the company could pay its interest Debt; higher is better in this case. Let’s say that my cousin’s company, Mini Food’s Inc. owes me $100. I decide to give her 10% percent interest, that means she owes me $10 for the first year's’ interest payment. Her company earns $130 per year. So with $130 of earnings versus $10 of interest her Interest Coverage ratio is 13. That means that she can pay the annual 10% interest for 13 years just off of this year’s earnings.

Hopefully that makes a little more sense, so let’s look at another example. For a stock, you have to find the pre tax earnings and then add the interest expense. That will give you the EBIT, or the Earnings Before Interest and Taxes. After that you have to divide the EBIT by the interest expense and that will tell give you the answer to the ratio. Now we’ll look at a real life example.

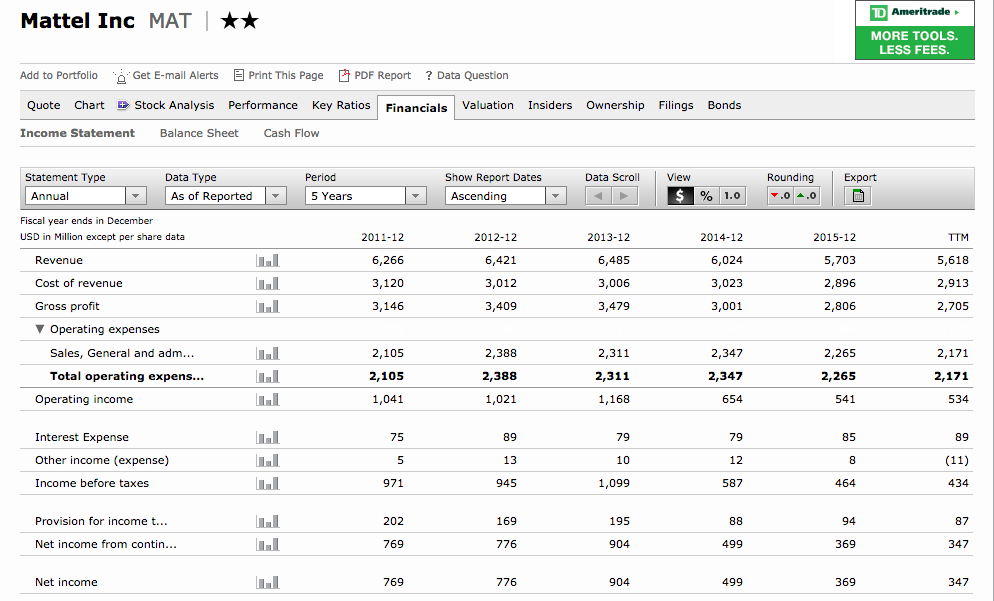

Let’s look at Mattel. Their pre tax earnings are $347M so we want to add that to $89M, for an answer of $436M. That means that the EBIT is $436M. Next, we will divide the EBIT by $89M, the interest expense. The answer is 5. That means just from this year's profit Mattel can pay 5 years worth of their Debt.

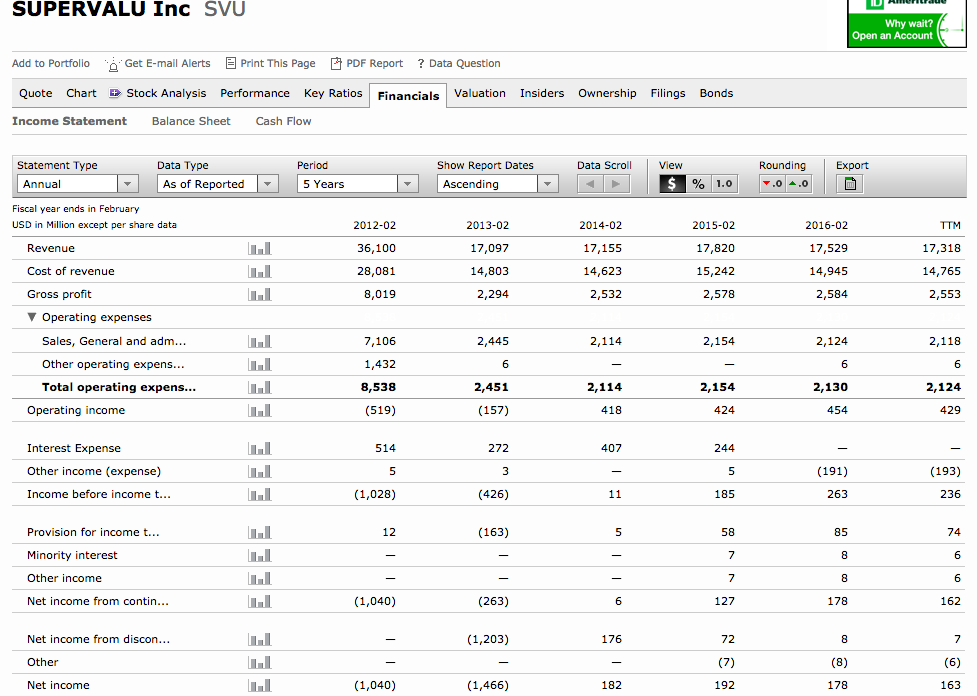

It’s always good to add in an example of what not to look for, even for risky investors this stock is a no-go. We are going to look at a company called SuperValu it’s a grocery store that got itself into a predicament. They are having a bankruptcy problem so they don’t have a Interest Expense, that means the data I’ll be using is from 2015 Their pre tax earnings are $192M next we add that to $244M, that gives us $436M. Now we divide that by $244M. The Interest Coverage Ratio is 2, please note that it’s rounded the exact answer is 1.7. It’s funny that Mattel and SuperValu had the same EBIT but their Interest Coverage Ratio is very different. Both earn the same, but Mattel investors get more earnings and have to make way less debt payments.

The last question about Debt is “Why should investors care?” Here is a great bit from an interview between Tom Gayner from Markle and an investor. It makes Debt really make sense. You can understand why it’s a dangerous and important thing.

“If you’re looking to buy businesses, don’t buy businesses where they use a lot of Debt. And I wondered why. And he said, well, if you want to make sure that you’re dealing with high-quality, high-integrity people, generally speaking, high-quality, high-integrity people don’t use a lot of Debt. Or not so much that, but if you’re a bad person, if you were sort of a little bit of a crook or had a little bit of larceny in your heart, it’s unlikely that you would use 100% equity finance. Because when it’s equity financed it means it’s your own money. When it’s Debt, you’re running your business on other people’s money. He says crooks don’t steal their own money, they steal other people’s money. So when you see a business that sort of relies on a bunch of Debt to operate and be successful, that adds a layer of concern or diligence that you have to do, you have to think about, that you don’t have to do if you look at a business that just doesn’t use much Debt. So it’s a margin of safety. That’s a word and a phrase that Ben Graham used quite a bit in thinking about investing, by looking at companies that don’t use much Debt. That really protects your downside and protects you from bad things happening."

Just because a company has Debt does not mean they are crooks. I like everything about that quote with the exception of one thing, he uses the word crook. They aren’t necessarily crook’s per se. Yes, they are spending and sometimes wasting other people’s money but just because a company has Debt in no way means they are crooks. It means that the company is more or less risky. So for that reason for the rest of this post I am going to substitute the word risky for the word crook.

Legit Companies

|

Risky Companies

| |

Has Debt

|

X

|

X

|

Low/No Debt

|

X

|

*** The “X’s” mean that it is a possible option***

As you can see a Legitimate Company will get out of Debt, because they work hard and are not doing all that just to make money. Legitimate companies know to run a company. Hard working companies sacrifice a lot and really have to believe in it. The Risky Companies are normally run by people who think all you need is money and the hard work happen itself. I think we all know that’s not how it works.

Comments

Post a Comment