On December 26th, 1993, Robert Gaughen took over Hingham Institution for Savings as CEO during a tumultuous time for the bank. A former Hingham president was arrested on charges that the illegally approved loans costing the bank millions, and for which he allegedly received $240,000 in illegal payments.

The bank was also underperforming. Non-Performing Assets were $9.4 million in 1992, 6.2% of assets, which were quickly reduced by 90% to $0.9 million, 0.62% of assets, in 1994, and only continued to improve from there. Asset quality is critical to the survival of a bank, and along with these improvements, Hingham began paying a dividend in 1994.

*Source: Hingham Institution for Savings’s 1994 Annual Report

Over the next 26 years, the company’s loan quality improved, its branch network expanded outside of Hingham, Massachusetts, and Book Value per Share grew 14 times. The company’s share price has grown 15.6% per year (including dividends).

*Hingham Institution for Savings’s 2018 Annual Report

Robert Gaughen reduced loans to lines of business such as speculative construction and installment lending and restructured personal loans. Throughout that time, he worked to refocus the bank by anchoring their business in higher quality lending like commercial real-estate lending. This allowed the bank to gain momentum and establish the markets they serve through to today.

Let’s take a deeper look into Hingham Institution for Savings and Robert Gaughen’s leadership.

Hingham Institution for Savings (later referred to as HIFS) came from humble beginnings. It was originally opened in 1834 without a building. At that time deposits were accepted in a David Harding’s general store in Hingham one day a week. Then they expanded to one branch in Hingham where they are headquartered today.

As the bank’s performance worsened in the early 1990s, Robert Gaughen, his father, and a few other HIFS directors/investors wanted change. They formed a group and proxied to force the resignation of HIFS’s president and install a new slate of directors. The dissident group successfully acquired a 33% stake in HIFS and won the proxy battle.

After Robert Gaughen won the proxy fight, he was faced with the challenge of building a team, because only a small number of key employees remained with the bank. The commercial lending staff, residential lending team, and CFO were replaced within a year along with turning over the Board of Directors even if they were not standing for re-election. As Robert Gaughen was reestablishing the bank, the Vice President of Administration, Bill Donovan, became a key player in creating a positive reputation for Hingham Institution for Savings because of his extensive knowledge on the operational staff.

Similar to Cera Sanitaryware, and many other intelligent fanatic-led businesses, Robert Gaughen remained hyper focused on a small market, Boston’s South Shore. 1995 marked their first expansion to towns nearby the Hingham area and they remained nearby for the next decade. HIFS stayed focused on their core community and opened another branch in the local retirement home.

Further growth was calculated. After 13 years as CEO, Robert Gaughen opened a branch in Boston (~20 miles to the North). HIFS was very active in the Boston area prior to opening a branch there. Boston posed an attractive market for HIFS to invest their capital in the high-quality real estate that they specialized in. Seven years after their first branch in Boston opened, HIFS expanded to Nantucket, a small island off of Cape Cod. Relationships that Robert Gaughen built in South Shore and Boston helped form a community of customers in a not so competitive but affluent market.

By expanding to Nantucket, HIFS realized that they were able to operate at a distance from their headquarters. This gave them the confidence to expand into Washington, DC. Where Boston is a highly competitive market with approximately 20 banks operating in that area, DC is a simpler marketplace for Hingham to establish itself in. However, in many other ways DC is quite similar to Boston with long term prospects, a size that is easy to operate in, a capacity to reinvest, and an ownership structure that HIFS was comfortable with and experienced operating in.

The key to the company’s success has been its culture. His son, Patrick Gaughen, current President and COO of HIFS, says, “We are focused on finding exceptional people and creating the conditions for them to do what they enjoy doing, well. It means maintaining stable strategic priorities which in turn providescultural stability - i.e. we focus on our customers and finding ways to improve the business, rather than on internal politics, or the new business priority du jour, or disruptive M&A, all of which are problematic and distracting for excellent people. Our ownership structure and the family involvement really helps on this point. We hire relatively slowly and try to maintain a very high bar for people that join the team, as great players enjoy playing with other great players.”

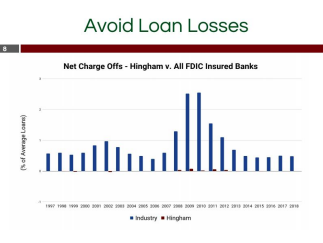

HIFS’s leadership and culture engendered organizational efficiency. In Hingham’s 2001 Annual Report Robert Gaughen said, “Our cost control efforts also continued to produce one of the best efficiency ratios among our peers. We continue to spend less while producing more.” Throughout their many expansions, HIFS’s Net Charge Offs have remained nearly invisible compared to the industry, and their Efficiency Ratio reached an all-time low at 29.89% making them one of the most efficient banks in the country. As they continue to expand, HIFS stayed true to its business roots by not going into industrial sectors just so they can expand. Robert Gaughen said in the 2014 annual report, “Balance sheet growth at Hingham must be safe and it must be profitable, in that order.”

*Source: Hingham Institution for Savings’s 2018 Shareholder’s Meeting

Even in the face of the Great Recession HIFS only continued to grow, the bank added $53 million of loans, approximately 9% growth while many other banks faced dire straits. HIFS’s focus on its customers worked in its favor more during the Recession than ever. In their 2009 annual report, Robert Gaughen said, “Our soundness as a bank has resonated with many of our new customers. Their disappointment with the larger banks continues to provide us with new opportunities to develop these relationships.”

Larger banks were involved in risky real estate opportunities or were not as involved in their marketplace which allowed HIFS, a bank in a position to lend, to grow.

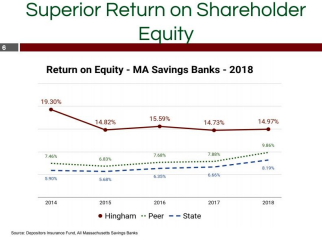

Looking at profitability, their rolling five years Return on Equity (ROE) is 15.92% which is an average of 7 points above HIFS’s competitors and 9 points above the Commonwealth of Massachusetts banks. In banks, ROE in an important metric to measure because it shows the success and productivity of the management at earning a return. Consistent double-digit ROE is rare in the banking industry, and HIFS has a long track record of exceeding it.

* Source: Hingham Institution for Savings’s 2018 Shareholder’s Meeting

While HIFS continues to expand, grow, and establish itself in other areas on the East Coast, they remain connected with and committed to supplying credit to their community. HIFS’s size allows them to invest in their community in ways which larger banks would not be able to do while exercising discretion. Although HIFS values the community it has helped grow, they realize that there are natural limitations to retail and capital that exist in South Shore. This resulted in the bank expanding to other areas that are structured similarly to markets they know well and thrive in.

HIFS’s latest expansion is to mobile banking which allows them to address more customers at a lower cost and is highly scalable. In our interview, Robert Gaughen said, “We need to be cognizant of the fact that technology makes us stronger and faster than one might have anticipated five years ago. Folks no longer visit the bank in the way that they once did, so being local and being in a variety of different locations is not as important as having quality technology, and that is a big change.” Mobile banking is also where Hingham competes with bigger banks. They are able to cover their customers wherever life may take them, and by investing in customer-facing improvements they can take cost out of their business. “Our model - personalized service, combined with digital excellence and low fees - is the future of our industry,” said Robert Gaughen in Hingham’s 2017 Annual Report.

Robert Gaughen added, “I am lending to people my dad lent to”, and now his son, Patrick Gaughen, is doing the same. Patrick Gaughen has worked to build a team at HIFS with a skill set to take the company forward. Patrick Gaughen’s strengths are exactly what the bank needs to continue its success. He has a background in computer science which will help progress the already successful mobile banking aspect of Hingham, and his “favorite place where life takes him” just happens to be DC, a new home for HIFS.

However successful their history has been, there are of course risks that can occur with time: Appealing to the next generation of customers, new regulations in the banking industry, and maintaining HIFS’s valued culture. There are also new competitors; First Republic is one of the main and “capable” competitors for HIFS in some of their segments. HIFS’s personalized approach to banking will have to continue to deliver and appeal to customers in order to defend its moat.

HIFS has been around for close to 200 years, but the most exciting may be to come. Robert Gaughen established the foundation in 1993, succeeded as a small bank during financial crises, and delivered excellent long-term returns. HIFS’s future will be determined on its ability to improve on the things it does well in efficiency and quality while delivering in new marketplaces and technologies.

(This was originally posted Sept 2019 on Ian Cassel and Sean Iddings' Intelligent Fanatics site.)

Nice work!

ReplyDeleteHello Blog admin I want to share some useful articles here for anyone looking for financial help to get through.

ReplyDeleteI want to talk about a God Fearing loan lender who lend me $400,000.00 to finance my business when I couldn't get help from my community bank here in Ohio, Mr Pedro was very nice to work with in every aspect of financial assistance so I will advise anyone here looking for a loan to contact Mr Pedro on Email / WhatsApp text.

Pedro Email: pedroloanss@gmail.com

Mr Pedro WhatsApp text: +1 863 231 0632

Portugal golden visa properties

ReplyDeleteMy Golden Pass brings to you below list of Portugal golden visa properties 2023. These properties are eligible for Golden Visa under the new rules announced in January 2022. You can read our blog on Portugal Golden visa new rules here.