The importance of saving is a concept many people struggle with, but the struggle of saving is more prevalent in teenagers of our society. About 57% of Americans have less than $1,000 in their savings accounts, with the average amount of money in a checking account being $4,436. Most teenagers don’t even have anywhere near that kind of money, but they have enough to visit the vending machine one to two times a day. This post is meant to open one’s eyes to the power of compounding. Let’s talk about my friend Ryan.

Ryan visits the vending machine about once a day. With a range of snacks from a Coca-Cola to a Hershey chocolate bars with a low initial cost of $0.75 to $1.50, the vending machines are quite hard to resist. On an average day, Ryan will spend $2.25 on a bag of gummy bears ($1.25) and a Diet Snapple ($1.00). For a midday snack, it isn’t a bad price, but over time it can add up. If Ryan spent $2.25 everyday for two months of school days (40 days) it totals to $90.00. That was a little anticlimactic (I swore it would be a higher total). Even still with $90.00 you can buy a tablet, Polaroid camera, T.V. monitor or about seven and a half copies of Early Bird: The Power of Investing Young. To make my point even stronger let’s say Ryan bought his favorite snack for the rest of his high school career (4 years). That would total to $2,160, a.k.a. too much money to spend on a vending machine.

I am not bashing Ryan’s snacking, so let’s see how he could put a positive spin by going on a spending diet. Let’s see what happens if he saved on snacks and chowed down on compound interest. Assuming Ryan retires at age 65 and starts investing in a stable company now (age 15) with an annual compound growth rate of 10% his money could grow and grow.

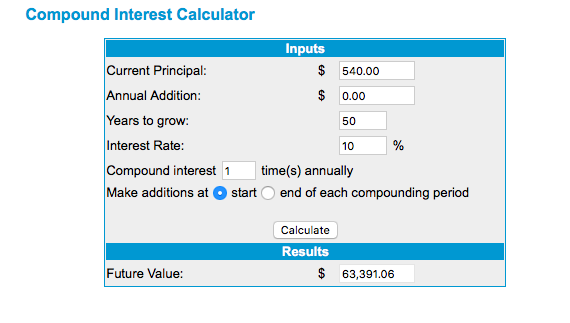

Using Moneychimp’s compound interest calculator, we can see the value of an initial investment of $540.00 (a year’s worth of snacks), compounded over 50 years (about the time it would take him to retire). Ryan’s money would’ve compounded to $63,391.06. I don’t know about Ryan, but I would much rather have $63,391.06 in 50 years than a few snacks today.

Finally if Ryan took the $1.50 he spent on a candy bar and invested it with the same time frame and interest rate, he would make $176.09. Would you rather please your taste buds right now or get an extra $174.59 50 years from now?

Comments

Post a Comment