We commonly compare two similar companies, but what if we were to look at two polar opposites? Tiffany (TIF) and Dollar Tree (DLTR). Tiffany is a high-end jewelry company. They sell jewelry anywhere from $25 to $200,000. Now, Dollar Tree, that’s a different story. All their products are a dollar or less, selling anything from socks to pencils. Both companies are reasonably profitable, with margins over 25%. These companies sell to different consumers, and they are both targeting two different sides of the market.

We commonly compare two similar companies, but what if we were to look at two polar opposites? Tiffany (TIF) and Dollar Tree (DLTR). Tiffany is a high-end jewelry company. They sell jewelry anywhere from $25 to $200,000. Now, Dollar Tree, that’s a different story. All their products are a dollar or less, selling anything from socks to pencils. Both companies are reasonably profitable, with margins over 25%. These companies sell to different consumers, and they are both targeting two different sides of the market. Dollar Tree is trying to offer cheaply priced products for their customers and easy to reach with 13,600 stores in the U.S. and 226 stores in Canada. They are trying to expand in Canada to have 1,000 stores in total. This may be a problem, Dollarama is a large competitor in Canada. Dollarama already has over 1,000 stores developed in Canada. If Dollar Tree was to be successful enough and get past this competitor that would not be the end of their troubles. They bought their main U.S. competitor, Family Dollar. Just like in the U.S. they would have to deal with Target, Walmart and other businesses competing for the same target crowd. Dollar Tree has one thing to its advantage, all their products are a dollar. Family Dollar, which is like a CVS or Walgreens, without the drugs, but with 20% lower prices. Family Dollar is not as cheap as Dollar Tree but still reaches the “Cost Advantage” moat. Because of this, they can have two similar target markets. This makes Dollar Tree indestructible to a large competitor, Amazon.

Tiffany, on the other hand, is trying to maintain their high end, an expensive

reputation that they have maintained since 1837. Unlike most stores, Tiffany prides itself on their different type of layout. Instead of having the cheaper items in the front, drawing more customers in, they put their most expensive products up front to retain their lavish brand. Somewhat recently, Tiffany has raised their dividend by 11%. It went from the previous 45 cents to 50 cents per quarter. This is the 16th time in the last 15 years that it has been raised.

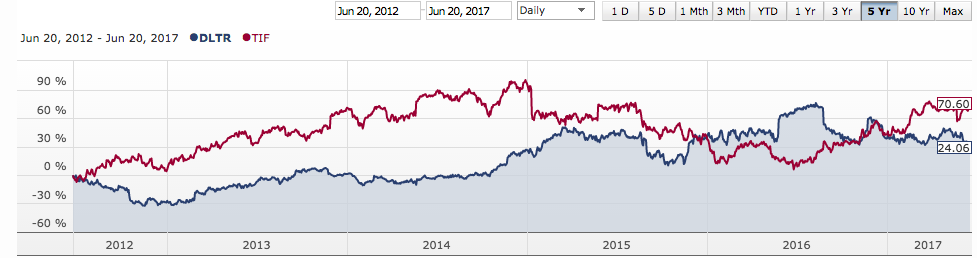

Now that we have established what the future holds for each company we have to choose, do we want a ring pop or an 18k gold, diamond ring? This is incredibly tricky to do, even just thinking about the analogy. Overall, Tiffany and Co’s stock has made more growth, at it’s highest point 90%. Whereas Dollar Tree’s 70%.

Once, we have looked at their future and past, let’s compare their current position.

Companies

|

Price To Earnings

|

Dividend

|

Gross Margin

|

Return on Equity

|

Debt

|

Tiffany and Co

|

25.6

|

2.00%

|

62.4%

|

15.0%

|

0.3

|

Dollar Tree

|

18.9

|

---

|

30.9%

|

16.8%

|

1.1

|

Starting with the P/E Ratio, neither has a bad one. As I’ve mentioned before, it isn’t bad to pay a little more for a good company, but a higher P/E Ratio means fewer earnings for your investment dollar. Not having a dividend is not a total loss, but it’s nice to have. Comparing the numbers, Tiffany looks like a better candidate because their Margins are better, they have a Dividend and less Debt.

Last, but not least, their moats. We are going to start with Dollar Tree. Dollar Tree has Cost Advantage. Looking at their name you can see that is the moat they pride themselves with and is most beneficial to their company. They also have Intangible Assets because of their brand. Those are both very powerful advantages. An easy way to tell if a moat is working is by the company’s Margins. Tiffany only has Intangible Assets, but that is extremely powerful in their case. Because of their brand, customers are willing to pay 30% more for their products because of their brand name. On the other side, Dollar Tree’s moat is Cost Advantage their Margins remain high, which is great. It also isn’t bad if the margins are low if the company can run and deal with supply and demand at low costs. If you ever need to check the success of a moat look at the Margins.

All in all, Tiffany has shown a stable past, good margins and numbers, reliable moats and a hopeful future. This should in no way change your opinion, there are different companies for different people. I believe both companies will be successful in the future but see Tiffany as a great company.

Comments

Post a Comment